The defining feature of the independent sponsor model is also its hardest problem. You sign a letter of intent first. You raise the capital second. This page explains how capital for independent sponsor deals comes together, who provides it, what is changing, and how successful sponsors differ from sponsors that fail.

The typical 90-day exclusivity window starts the moment the seller accepts your LOI. Inside it, you run diligence, line up lenders, paper the deal, and assemble an equity syndicate that did not exist when you made the offer. Soft commitments come in. Some convert. Others vanish into new mandates, sector changes, or capital partners who simply go quiet. The seller is watching the clock. So are the brokers who control your next three deals.

If you’re raising equity for a deal under LOI

CapitalPad is a private equity co-investment group focused on independent sponsor transactions. We typically commit $1M to $2.5M of equity per deal, backed by accredited investors aggregated into a single SPV alongside participating funds and family offices.

Typical fit: a profitable U.S. or Canadian company with $1M to $7M of EBITDA, $5M to $30M of enterprise value, and a signed LOI. No cost to sponsors at any stage.

Learn more →Capital formation, not deal sourcing, usually determines whether a sponsor builds a career or burns out after one or two failed transactions. A sponsor who cannot reliably raise capital within the exclusivity window loses deals, strains relationships with sell-side advisors, and eventually runs out of opportunities. A sponsor who has solved the capital problem moves faster, wins more competitive processes, and builds the track record that makes each raise easier than the last.

The Short Version

- The independent sponsor capital raise runs in parallel with diligence, debt financing, and legal documentation inside a 60 to 120 day exclusivity window. Most sponsors who fail at the model fail here, not at sourcing.

- Family offices lead 27 percent of independent sponsor deals and appear in 62 percent of capital stacks. Historically, they are the most important single source of equity capital in the segment.

- Institutional capital remains structurally underweight at roughly 11 percent of capital, primarily because check sizes are too small and underwriting timelines are too short for most institutions.

- Junior debt usage has declined from 81 percent of deals in 2023 to 61 percent in 2025 as sponsors became more conservative in a higher-rate environment. Senior debt and seller notes are now the dominant financing instruments.

- 32 percent of independent sponsors cover broken deal costs entirely on their own. The risk allocation depends heavily on the stage of the transaction and the formality of the capital partner relationship.

- Dedicated independent sponsor co-investment vehicles closed by Global Endowment Management ($450M+), and HighVista Strategies ($800M) have changed the capital provider universe over the past two years. Independent sponsor co-investment groups like CapitalPad aggregate accredited investor commitments into a single SPV per deal, giving sponsors access to a larger investor base without managing dozens of individual relationships.

How the Independent Sponsor Capital Raise Actually Works

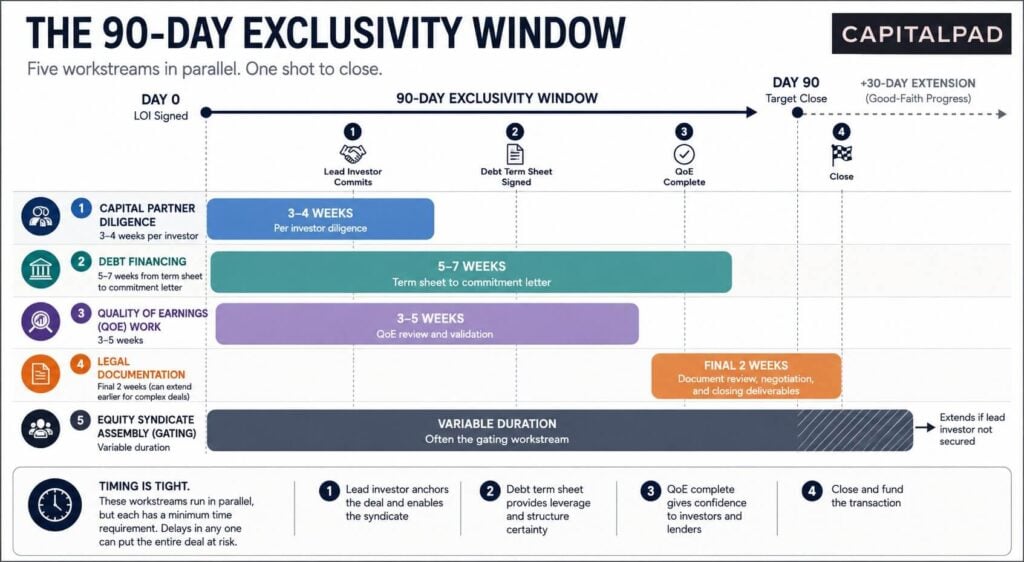

More than 1,500 active independent sponsors now operate in the United States, roughly double the count of five years ago.1 Every one of them has had to solve the funding problem to survive, and the sequence is generally the same on every deal. A sponsor signs an LOI with a target seller. The exclusivity window starts. Three workstreams run in parallel for the next 60 to 120 days: diligence, debt financing, and equity raise. Legal documentation runs alongside all three.

Here’s a chart on the general timing of independent sponsor deals

The 90-day window most commonly includes a built-in 30-day extension on good-faith progress. Inside that window, each workstream has its own minimum time requirement:

- Capital partner diligence: 3 to 4 weeks per investor

- Debt financing: 5 to 7 weeks from term sheet to commitment letter

- Quality of earnings work: 3 to 5 weeks

- Legal documentation: At least 2 weeks at the end, generally longer

- Equity syndicate assembly: Variable, often the gating workstream

The math is tight, and that is on a deal where nothing goes wrong.

The Lead Investor Dynamic

The equity raise typically begins with a lead investor. The lead is the capital provider who commits the largest single check, anchors the deal, often takes board representation, and signals credibility to other co-investors.

Without a credible lead, the rest of the syndicate is slow to form. With a credible lead, the syndicate forms around them. Once the lead is in place, the sponsor brings in additional co-investors to round out the equity stack. Each new investor performs their own diligence, which is why the timeline pressure inside the exclusivity window is real.

Why Soft Commitments Fail

“Soft commitments do not always convert” is the single most important phrase in independent sponsor capital formation. A capital partner who expressed enthusiasm during initial conversations may, by the time you call them in week six to finalize their commitment, be focused on a different deal, no longer interested in your sector, or simply unresponsive.

The sponsor who has only two or three capital relationships is one vanished commitment away from failure. The sponsor who has cultivated eight to ten relationships has redundancy.

Who Provides the Equity Capital

The composition of the independent sponsor capital base has changed materially over the past five years, but the rank order of capital sources has stayed roughly constant. The 2024 McGuireWoods Independent Sponsor Deal Survey2 shows the following distribution among lead investors:

- Family offices: 27 percent of deals

- Mezzanine and equity funds: 25 percent

- Private equity funds: 19 percent

- High net worth individuals: 16 percent

- Institutional investors: 5 percent

The 2025 Citrin Cooperman Independent Sponsor Report3 measures a different cut of the data. Looking at which capital sources appear anywhere in the capital stack, family offices appear in 62 percent of deals, high net worth individuals in 55 percent, SBIC funds in 53 percent, and mezzanine funds in 45 percent. The two surveys are measuring different things, but the picture is consistent. Family offices, mezzanine providers, and SBICs are the working capital base of the segment. Institutional capital remains a small share.

Capital Source Comparison

| Capital Source | Typical Role | Why Sponsors Use Them | Main Trade-Off |

|---|---|---|---|

| Family offices | Lead investor or large co-investor | Flexible decision-making, sector knowledge, longer hold tolerance, meaningful check sizes | Highly idiosyncratic preferences and relationship-driven access |

| Mezzanine and equity funds | Debt provider, equity co-investor, or lead capital partner | Predictable process, defined check sizes, ability to combine debt and equity | More structured underwriting and less flexibility on terms than family offices |

| SBIC funds | Subordinated debt and equity capital provider | Well-suited to lower middle market deal sizes and flexible capital stacks | Program rules, eligibility limits, and underwriting constraints |

| Private equity funds | Lead investor or structured capital partner | Can provide credibility, larger checks, and repeat capital | May seek more control, stronger economics, or future platform ownership |

| High-net-worth individuals | Smaller co-investors | Useful for filling out equity stacks and building sponsor relationships | Administrative complexity if not aggregated through an SPV |

| Co-investment groups | Aggregated investor base through a single SPV | Clean cap table, broader accredited investor access, lower administrative burden | Sponsor presents each deal to the group rather than relying on a pre-committed pool, which adds a review step |

Each category warrants more detail, particularly on how sponsors actually work with them in practice.

Family Offices

The most important single source of independent sponsor equity. Several structural advantages over other capital providers:

- Speed. Can move quickly on deal-by-deal decisions because they have not built committee-driven institutional processes.

- Hold period flexibility. Can hold for longer periods than fund vehicles, which matters when sponsor deals stretch to seven or eight year holds.

- Operating experience. Often have sector expertise that makes diligence more substantive and post-close support more valuable.

- Meaningful check sizes. Single-family offices regularly commit $2M to $10M to individual deals.

The trade-off: Family offices are highly idiosyncratic. Each has its own preferences on sector, geography, deal size, governance, and economics. A sponsor with twenty family office relationships may find only three are right for any specific deal. Discovery is slow. Relationship cultivation is personal. Deal-by-deal fit varies materially.

Mezzanine and Equity Funds

The second largest lead investor category and the most consistent capital source across deals.

- Typically take a strip of equity alongside their mezzanine debt position

- Simplifies the capital stack and creates aligned incentives on equity value creation

- Institutional processes, defined check sizes, clearer sector preferences than most family offices

- Predictable timelines, which makes them useful anchors for sponsors trying to close inside exclusivity

SBIC Funds

SBIC participation increased by 19 percentage points over the three years through the 2025 Citrin Cooperman survey. Three reasons SBICs work well in the lower middle market:

- Can take both equity and subordinated debt positions in the same deal, giving sponsors a one-stop capital partner

- SBA leverage program allows roughly $2 of borrowed capital for every $1 of equity, expanding effective check size

- Specifically designed for the deal sizes most independent sponsors target

Private Equity Funds

Roughly 19 percent of deals as lead investors. The participation pattern has changed materially.

Five years ago, most PE funds backing independent sponsors did so opportunistically. Today, several have built dedicated independent sponsor programs with named teams, defined economics, and ongoing pipelines. Fidus, Trivest (through its Discovery Fund), and Peninsula are among the more visible examples. The growth of these dedicated programs is one of the most consequential trends in the segment.

High Net Worth Individuals

Appear in 55 percent of capital stacks but lead only 16 percent of deals. Most commonly co-investors who participate alongside a lead family office or fund.

This is the segment where the rise of co-investment groups has had the most impact, because aggregating $25K to $100K individual checks into a single line item solves a meaningful administrative problem for sponsors.

Why Institutional Capital Is Underweight

The 5 percent figure for institutional lead investors and 11 percent figure for institutional capital share are striking, given that institutional investors dominate the rest of the private equity market. Three structural reasons explain the underweight:

Check Sizes Are Too Small

A typical independent sponsor deal has total equity of $5M to $30M, with individual investor checks ranging from $1M to $10M. A large institutional LP that deploys $25M minimum tickets cannot efficiently participate in a deal that only needs $15M of total equity. The math does not work, regardless of how attractive the underlying opportunity might be.

Underwriting Capacity Is the Constraint

Traditional institutional LP teams underwrite manager commitments, not individual deals. Evaluating an independent sponsor transaction requires deal-level diligence on the target business, the sponsor’s capabilities, the capital structure, and the post-close plan, which takes the same time as underwriting a full fund commitment but produces a much smaller deployment.

Risk Frameworks Favor Diversification

Institutional governance generally requires portfolio-level risk management, which is difficult to achieve in a deal-by-deal structure. A commitment to a committed fund spreads exposure across 15 to 20 companies. A commitment to a single sponsor deal concentrates exposure in one company. Most institutional risk frameworks penalize the latter, even when the underlying economics are better.

The implication for sponsors is that institutional capital is a slow and limited piece of the puzzle for most deals. The exception is the rise of dedicated independent sponsor co-investment funds, which solve all three problems by aggregating institutional capital, building dedicated underwriting teams, and producing portfolio-level diversification.

The Debt Side of the Capital Stack

The debt component of the capital stack matters as much as the equity, and the patterns have shifted meaningfully in the past two years.

Current Financing Mix

Axial’s 2025 Independent Sponsor Report1 shows the following financing structures across recent deals:

- Senior debt: 85 percent of deals. Largest single component of most capital stacks.

- Seller notes: 60 percent of deals. Growing as a tool for bridging valuation gaps.

- Junior debt: 61 percent of deals, down from 81 percent in 2023.

- SBA loans: 30 percent of deals. Particularly useful below $15M enterprise value.

- Earnouts: 33 percent of deals, down from 44 percent in 2023.

The Junior Debt Decline

The decline in junior debt usage is the most consequential trend. Higher interest rates have made junior debt less attractive because the cost of capital has risen faster on subordinated debt than on senior debt.

Sponsors who five years ago might have funded a deal with 4.0x senior leverage plus 1.5x junior leverage are now more likely to fund it with 3.5x senior leverage and a larger equity check. The shift reduces enterprise risk but compresses sponsor and investor returns relative to the higher-leverage structures of the prior cycle.

Seller Notes as Valuation Bridges

Seller notes have become a critical tool for bridging valuation gaps. A seller who wants a 6.0x EBITDA multiple but is offered 5.0x can be bridged with a seller note that pays out the difference contingent on continued business performance.

The tool works because it shifts some of the valuation risk back to the seller and gives the sponsor flexibility on the cash purchase price. The 60 percent prevalence reflects how routinely this tool is now used.

The Debt-Equity Timing Problem

Senior lenders typically want to see committed equity before they will fund debt. Equity investors typically want to see committed debt before they will fund equity. Both sides looking at the other side is a recurring source of delay inside the exclusivity window.

Working sponsors solve this by having debt term sheets in hand before they sign the LOI, even if the term sheet is non-binding. This gives them something to show equity investors and substantially reduces the “you go first” dynamic.

Broken Deal Costs and Warehousing Risk

Not every deal closes. Diligence reveals issues. Financing falls through. Sellers renegotiate. Lenders pull commitments. Material adverse changes happen. The result is broken deal costs, and the allocation of those costs is one of the more important and least discussed parts of the independent sponsor model.

The Allocation Pattern

The Citrin Cooperman 2025 survey3 shows that 32 percent of independent sponsors cover broken deal costs entirely on their own. The 2022 McGuireWoods survey shows that 61 percent of control buyouts had equity providers covering all broken deal costs once formally partnered with the sponsor.

The two findings are consistent if you read them carefully. The allocation depends heavily on when the deal breaks.

- Before formal capital partner selection: Sponsor bears all costs. Legal fees, accounting fees, diligence consultant fees, and the sponsor’s own time are sunk costs.

- After formal capital partner selection: Cost allocation usually shifts. In single-investor control buyouts, equity provider typically covers all costs from the date of the formal partnership letter.

- Multi-investor syndicates: Costs may be shared pro rata across committed investors, often with a defined cap on sponsor exposure.

Typical Cost Magnitudes

- Clean deal that breaks early: $50K to $100K in legal and initial diligence costs

- Deal that breaks in mid-diligence: $150K to $300K

- Deal that breaks late, after QoE and full legal documentation: $300K to $700K or more

For a sponsor working on multiple deals over a year, broken deal costs can easily reach six figures in cumulative spend.

Warehousing Risk

A related issue that comes up in deals that close in tranches or that require the sponsor to fund operational needs between signing and closing. A sponsor who has personally guaranteed a transition services agreement, a key vendor contract, or a working capital line during the gap between signing and closing has personal capital and credit exposed.

Sophisticated sponsors push these obligations to the capital partner or to the portfolio company itself. Inexperienced sponsors often accept personal exposure that they did not fully understand at signing.

What Is Changing in the Capital Provider Base

The capital provider universe has expanded substantially over the past two years. Three developments matter most.

Dedicated Co-Investment Vehicles

- Global Endowment Management: Closed inaugural sponsor fund at over $450M on April 9, 2025, beating a $300M target with another $150M from affiliated vehicles4

- HighVista Strategies: Closed Fund XI at $800M on February 3, 2026, beating a $725M target5

These vehicles aggregate institutional capital, build dedicated underwriting teams, and produce portfolio-level diversification, which solves the structural problems that previously kept institutional capital out of the segment.

Dedicated Programs Inside Existing PE Firms

Fidus, Trivest, Peninsula, and others have built named programs with dedicated teams that specifically target independent sponsor deals. The programs typically offer faster decision-making, more flexible structures, and operating support that traditional PE backers do not bring.

Co-Investment Groups

Co-investment groups source, underwrite, and curate independent sponsor transactions, then aggregate accredited investor, family office, and fund commitments into a single SPV per deal.

CapitalPad operates in this space as a private equity co-investment group built for the independent sponsor model rather than committed-fund private equity. CapitalPad aggregates accredited investor commitments starting at $25,000 per investor into a single line item on the sponsor’s capital stack, which solves the administrative burden of managing dozens of small commitments while preserving the sponsor’s ability to present each transaction on its own merits. Unlike a placement agent, CapitalPad does not charge sponsors a fee for raised capital, which keeps the economic alignment with the sponsor clean.

The implication for sponsors is that the capital provider universe is now broader and more accessible than it was five years ago. The bottleneck is no longer “is there capital available.” The bottleneck is “have you built the relationships and reputation to access it.” If you are an independent sponsor running an active process, you can submit your deal to CapitalPad for review.

What Capital Partners Actually Look For

The flip side of the capital raise is the investor’s underwriting decision. Working sponsors understand what capital partners look for and structure their pitches accordingly. The companion piece to this article, how investors underwrite independent sponsor deals, walks through the underwriting framework from the investor’s perspective.

The Signals That Consistently Matter

- Sector expertise. Deep operating experience in the target sector is materially easier to back than generalist credentials.

- Personal capital in the deal. Rolling 50 percent or more of the closing fee into equity and putting additional personal capital in signals alignment. Maximum cash payout at close signals the opposite. Family office feedback in Axial’s 2025 report ranked sponsor capital at risk as one of the five most important factors in co-investment decisions.1

- A clean diligence package. Well-organized and internally consistent is a signal. Gaps and contradictions are a different signal.

- Realistic economics. Anchoring the economic ask to current market conventions makes the raise easier. Pushing aggressively on first deals creates capital partner skepticism that takes years to overcome.

- Co-sponsor or anchor investor. A first-time sponsor with a credible co-sponsor partially solves the track record problem. The co-sponsor model has become more common as the segment has matured.

What They Are Really Evaluating

Capital partners are looking for two things: sponsors who will produce returns, and sponsors who are easy to work with. The first factor is mostly about the deal and the sponsor’s ability to execute. The second is mostly about how the sponsor communicates, negotiates, and behaves under pressure. Both matter. Both can be signaled in the way the sponsor approaches the capital raise itself.

Practical Recommendations for Independent Sponsors

1. Build a Capital Partner Stable Before Signing LOIs

The single largest source of execution failure in the segment is the inability to convert soft commitments to actual closings within the exclusivity window. The only durable solution is a small group of capital partners with whom the sponsor has prior diligence relationships, established economic terms, and demonstrated trust.

- Three is the minimum.

- Five is more comfortable.

- Ten is unnecessary.

Building those relationships happens at the major independent sponsor conferences, through introductions from law firms and accounting firms active in the segment, and through direct outreach to family offices and funds that have backed sponsors in your sector. The work is unglamorous and takes a year or more to produce real depth. Sponsors who start the relationship building only after they sign their first LOI are too late.

2. Specialize by Sector

Sector-specialized sponsors generate measurably better deal flow, easier capital raises, and better realized returns than generalists. The compounding advantage of being the sponsor that owners and brokers in a specific industry call first is real and durable.

Specialization does not require a narrow vertical. Healthcare services, business services, light manufacturing, and home services are each broad enough categories to support a sponsor career.

3. Anchor Economics to Current Market Conventions

The 2 percent closing fee, 5 percent EBITDA management fee, and tiered MOIC carry structures documented in the McGuireWoods and Citrin Cooperman surveys are the working market.

Sponsors who anchor to these conventions on their early deals have an easier time raising capital and building trust. Sponsors who push aggressively on first deals often spend the first year of the partnership managing capital partner skepticism rather than executing on the business.

4. Address Regulatory Exposure Before the First Close

Transaction-based compensation can trigger broker-dealer registration considerations under Section 15 of the Securities Exchange Act of 1934. Multiple deal vehicles can approach Investment Advisers Act registration thresholds. These are manageable exposures, but only if addressed before the first close, not after.

Working with securities counsel familiar with private fund structures is not optional.

5. Document Broken Deal Cost Allocation Explicitly

Every capital partner relationship should have a clear written understanding of:

- When costs shift from the sponsor to the capital partner

- What the cap on sponsor exposure is during the pre-partnership phase

- What happens if a deal breaks after a commitment letter has been signed but before close

The conversation is uncomfortable. Having it before there is a broken deal is much easier than having it after.

What Good Looks Like

A sponsor who has solved the capital problem looks the same way across deals:

- Small group of capital partners they have worked with before

- Knows which partners take leads and which prefer to co-invest

- Debt term sheets in hand before signing LOIs

- Clean diligence package ready to share within 48 hours of LOI execution

- Explicit written agreements on broken deal cost allocation

- Securities counsel reviewing deal vehicles

- Realistic economic asks anchored to current market conventions

- Clear story about why they are the right buyer for this specific business in this specific sector

The sponsor who has not solved the capital problem looks different. Constantly hunting for new capital partners. Surprised by how long diligence takes. Scrambling to convert soft commitments late in exclusivity. Absorbing broken deal costs they did not expect. Negotiating economics from a weak position because they have nowhere else to turn. Losing deals to better-organized sponsors.

The difference between the two is not talent. It is preparation, relationship building, and the willingness to do the unglamorous infrastructure work that capital formation requires.

Independent sponsor investing has matured to the point where the capital is available, the conventions are recognized, and the infrastructure exists to support deal-by-deal execution. The sponsors who treat capital formation as a core competency rather than an afterthought are the ones building durable careers in the segment. The sponsors who treat it as an obstacle to deal sourcing are the ones who eventually wash out.

The capital problem is solvable. The sponsors who solve it are the ones who treat it as worth solving.

If you are running an active process and want to evaluate co-investment alongside your existing capital relationships, CapitalPad reviews deals on a deal-by-deal basis and aggregates accredited investor commitments into a single SPV that sits as one line item on your cap table.

Frequently Asked Questions

How long does an independent sponsor capital raise typically take?

The capital raise runs in parallel with diligence, debt financing, and legal documentation inside the LOI exclusivity window, which is most commonly 90 days with a 30-day extension. Capital partners typically require three to four weeks of dedicated diligence time, so working sponsors aim to have lead investor diligence underway within two weeks of LOI execution. Sponsors who start the capital raise after diligence is mostly complete are usually too late.

How many capital partner relationships does an independent sponsor need?

Three is the working minimum for a sponsor who wants reliable execution. Five gives meaningful redundancy. Ten is more than most sponsors can maintain meaningfully. The quality of the relationships matters more than the quantity. A sponsor with three deeply cultivated capital partners who know the sponsor’s deal criteria, have prior diligence relationships, and have established economic terms will outperform a sponsor with ten shallow relationships. Most relationships get built at the major independent sponsor conferences and through warm introductions from law firms and accounting firms active in the segment.

Who is the most important capital source for independent sponsors?

Family offices lead 27 percent of independent sponsor deals and appear in 62 percent of capital stacks. They have the speed, hold flexibility, sector expertise, and check size to anchor most lower middle market sponsor transactions. Equity funds and investment groups like CapitalPad are the second largest lead investor category and provide more predictable timelines, while SBIC funds have grown substantially as a one-stop capital source that can provide both debt and equity.

How does a co-investment group like CapitalPad fit into the capital stack?

A co-investment group aggregates individual accredited investor and family office commitments into a single SPV per deal, which becomes one line item on the sponsor’s capital stack. The model preserves the deal-by-deal selectivity that defines independent sponsor investing while solving the administrative complexity of managing dozens of small commitments. CapitalPad aggregates commitments starting at $25,000 per investor and does not charge sponsors a fee for raised capital, which keeps the economic alignment clean. Independent sponsors can submit a deal for review directly. The co-investment group model is one option among the broader set of capital sources, useful particularly for sponsors who want access to a diversified accredited investor base without building those relationships individually.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, tax, or financial advice. Independent sponsor deals involve significant risks, including loss of capital, illiquidity, and concentration. Market conventions and statistics discussed here are drawn from publicly available industry surveys and do not guarantee future results. Any investment or capital raising decision should be made in consultation with qualified advisors and based on the specific facts of the situation under consideration.

References

- Axial. 2025 Independent Sponsor Report.

- McGuireWoods LLP. 2024 Deal Survey of Independent Sponsor-Led Transactions.

- Citrin Cooperman. 2025 Independent Sponsor Report and related Uncharted No More series.

- Global Endowment Management. GEM Closes On Over $450 Million for Inaugural Independent Sponsors Fund. April 9, 2025.

- HighVista Strategies. HighVista Closes Oversubscribed Private Equity Fund XI at $800 Million. February 3, 2026.