Independent sponsors closed 27 percent of platform-sourced deals on Axial over the trailing twelve months covered in the 2025 Independent Sponsor Report. Traditional private equity funds closed 20 percent.1 The segment that operates without a committed pool of capital now drives more lower middle market deal volume than the segment with the institutional fundraising infrastructure to compete with it.

Most accredited investors and family offices still do not know how these deals work. They see a profitable lower middle market company, a motivated seller, a capable sponsor, and the ability to evaluate the exact acquisition before committing capital. That transparency is real. It is also easy to overvalue.

You are not just underwriting the company. You are underwriting the sponsor, the capital structure, the seller dynamics, the financing path, and the sponsor’s ability to actually get this transaction closed and run the business after closing. A good business with the wrong sponsor, too much debt, weak governance, or a vague post-close plan can still become a poor investment. This is the framework CapitalPad uses when underwriting the independent sponsor deals we invest in alongside accredited investors, funds, and family offices.

The right question is not, “Is this a good deal?” The right question is, “Is this sponsor, with this structure, buying this business at this price, with this capital stack and this plan, likely to produce an attractive risk-adjusted outcome?”

That is a harder question. It is also the point of deal-by-deal private equity. A blind-pool fund commitment is mostly a manager underwriting decision. An independent sponsor deal is a manager, company, structure, and execution underwriting decision, all at once.

This piece is a framework for evaluating independent sponsor deals before you commit capital.

Deal-by-deal access to independent sponsor transactions

CapitalPad is a private equity co-investment group focused on independent sponsor transactions. We give accredited investors access to curated lower middle market acquisitions, with co-investors aggregated into a single SPV alongside participating funds and family offices.

Accredited investors can participate on a deal-by-deal basis, with minimums starting at $25K per deal.

- EBITDA: $1M to $7M

- Enterprise value: $5M to $30M

- Geography: U.S. and Canada

- Structure: single SPV per transaction

The Short Version

- Evaluating an independent sponsor deal requires four separate underwriting decisions: the sponsor, the business, the capital structure, and the execution plan. Most weak analyses spend too much time on the business and not enough on the other three.

- Market terms have standardized. A 2 percent closing fee, 50 percent or more sponsor rollover, 5 percent EBITDA management fee with floor and cap, and tiered carry hitting 25 percent above 3.0x MOIC are now common market reference points. Deals materially outside these bands deserve scrutiny.

- The IRR versus MOIC hurdle choice is the most underweighted structural decision. MOIC hurdles do not penalize the sponsor for lengthening hold periods. IRR hurdles do. 50 percent of 2024 deals now use MOIC, up from 27 percent in 2019.

- Lower entry multiples are real. 54 percent of independent sponsor deals close below 6.0x EBITDA, compared with middle market PE medians between 10.2x and 14.9x.

- Dedicated co-investment vehicles like CapitalPad, Global Endowment Management, and HighVista Strategies solve the sourcing, access, and diligence capacity problem for investors who want segment exposure without underwriting every deal directly.

What You Are Actually Buying in an Independent Sponsor Deal

An independent sponsor finds a private company, signs a letter of intent, runs diligence, and then raises the equity and debt to close. The deal comes first. The capital comes second. You are not committing to a manager’s future pipeline. You are evaluating a specific named business with actual financials, diligence materials, and a real management team, and deciding whether you want exposure to this specific deal.

This inverts how committed-fund private equity works. A traditional buyout fund raises a blind pool, deploys it across fifteen to twenty companies over three to five years, and tells you the sector focus and the manager’s prior track record. You do not know the actual portfolio when you commit. Independent sponsor deals strip that out. Each commitment is a discrete underwriting decision on a known asset. You can pass on any deal for any reason.

The mechanical implications matter. The diligence you do is on the actual asset, not on a projected pipeline. Your alignment with the sponsor is direct, because the sponsor’s compensation depends on this deal performing, not on a diversified fund averaging the duds with the winners. And the structure self-selects for investors who want to think about each deal on its own merits, which is a meaningful filter on its own.

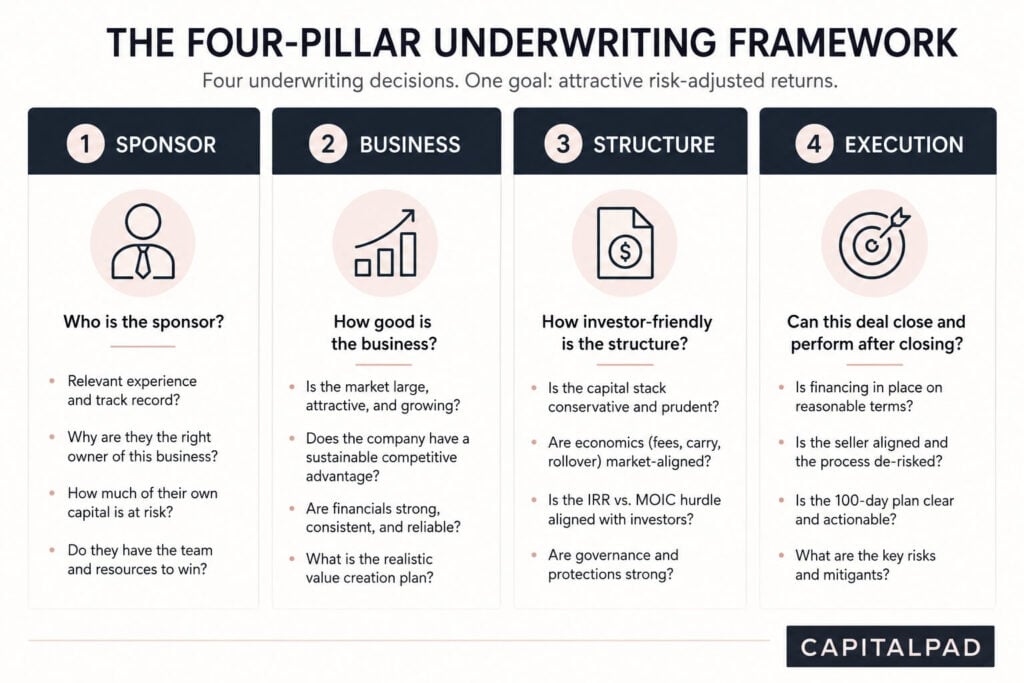

The Four Things You Are Really Underwriting

A serious investor breaks an independent sponsor deal into four separate underwriting questions:

- Who is the sponsor?

- How good is the business?

- How investor-friendly is the structure?

- Can this transaction actually close and perform after closing?

Most weak analyses spend too much time on the business and not enough on the sponsor and structure. That is backwards. In an independent sponsor deal, the sponsor is often the difference between a promising acquisition and a messy investment.

1. Underwrite the Independent Sponsor, Not Just the Deal

Access is not an investment thesis.

A sponsor who can find a deal but cannot explain why they are the right owner, how they will close, and what happens after closing has not solved your problem. They have introduced you to a new one.

The sponsor’s role is bigger than sourcing. They organize the transaction, coordinate debt and equity, manage seller communication, lead diligence, negotiate structure, support management, and oversee the post-close plan. Each of those steps can go wrong, and a sponsor who has not done them before is learning on your capital.

The signals that separate sponsors worth backing from sponsors that are not are not subtle, but you have to look for them.

Prior outcomes. If the sponsor has closed deals before, what happened. How did they perform. What went wrong. The most useful conversation is about the worst deal, not the best one. Sponsors who talk honestly about failure modes are easier to back than sponsors who claim every deal went exactly to plan.

Sector specialization. The 2025 Citrin Cooperman survey and broader industry data are consistent on this. Sector-specialized sponsors generate better realized returns and have measurably better access to proprietary deal flow.2 A sponsor who has spent five years in healthcare services has a network of operators, a working understanding of payer dynamics, and a list of warm targets that a generalist cannot replicate in any reasonable timeframe.

Personal capital in the deal. Look at the rollover percentage on the closing fee and any additional cash investment. Sponsors who roll 50 percent or more of their fee and put additional personal capital in are signaling alignment. Sponsors who minimize personal commitment and structure for maximum cash payout at close are signaling the opposite. Family office feedback in Axial’s 2025 report named sponsor capital at risk as one of the five most important factors in co-investment decisions, alongside track record, deal terms, industry relationships, and governance rights.1

References from prior capital partners and management teams. The relevant questions are about behavior during difficult periods, not victory laps during good ones. Did the sponsor maintain communication when distributions slowed. Did they take accountability when something went wrong. Did they treat co-investors fairly when they had leverage not to. These are the questions that separate sponsors you want to back from sponsors you do not.

The diligence package itself. Well-organized, internally consistent, and properly sourced is a signal. Gaps, contradictions, and unsupported assertions are a different signal. A sponsor who cannot produce a clean package is telling you something about how they will manage the business after close.

A sponsor with no meaningful capital at risk can still be capable. But the burden of proof is higher, and most of the time it is not met.

2. Underwrite the Business Like a Private Equity Investor

Most independent sponsor targets are not glamorous companies. They are profitable, founder-owned lower middle market businesses in fragmented sectors: home services, business services, light manufacturing, distribution, healthcare services, niche industrials, IT services, logistics, and other categories that fund decks call boring on purpose.

That can be attractive. It can also be dangerous if you romanticize simplicity. A simple business is not automatically a safe business.

The best independent sponsor opportunities have a specific type of imperfection. The company is good enough to own, but not so institutionalized that there is no room to improve it.

Good imperfections:

- weak reporting but strong cash flow

- underdeveloped sales process but strong customer relationships

- founder dependence that can be reduced with management depth

- regional fragmentation that allows sensible add-ons

- pricing discipline that can be improved

- systems that can be professionalized

Bad imperfections look superficially similar but behave differently:

- declining core demand

- customer concentration disguised as loyalty

- unsustainable margins

- weak middle management

- owner earnings that disappear after transition

- add-backs that do too much work

- debt capacity that only works in the upside case

The diligence questions that separate the two categories are not complicated. Is revenue recurring, repeat, project-based, or cyclical. How concentrated are customers. How dependent is the company on the founder. Are margins stable. Are add-backs credible. Is the management team real, or is the owner the business. Does the company have clean financial reporting. Is the industry fragmented for a reason that will continue, or for a reason that is about to resolve.

Do not ask only whether the company is profitable. Ask whether the profits are transferable, durable, and financeable.

3. Underwrite the Structure Before Underwriting the Returns

Projected returns are only as credible as the structure underneath them. Two deals with the same company, same purchase price, and same EBITDA can have very different risk profiles depending on how the capital stack and economics are arranged.

The economic structure has standardized over the past five years, which makes it easier to recognize when something is outside the normal bands. The 2024 McGuireWoods Independent Sponsor Deal Survey (more than 300 transactions)3 and the 2025 Citrin Cooperman Independent Sponsor Report (172 sponsor and capital provider respondents)2 document the conventions in detail.

| Term | Common Market Reference | Why It Matters |

|---|---|---|

| Closing fee | Often structured as a percentage of enterprise value, commonly around 2% of EV in many independent sponsor deals. | This is the sponsor’s upfront compensation for sourcing, structuring, and closing the transaction. Investors should focus on whether the fee is reasonable and whether a meaningful portion is rolled into deal equity. |

| Sponsor rollover | Many capital partners expect the sponsor to roll a meaningful portion of the closing fee, often 50% or more, into the deal. | Rollover is one of the clearest alignment signals. A sponsor with real capital at risk usually thinks differently than a sponsor taking most economics in cash at close. |

| Management fee | Often paid annually by the portfolio company, sometimes structured as a percentage of EBITDA with a floor and cap. | This compensates the sponsor for ongoing oversight. Investors should understand whether the fee reflects real post-close work or simply creates cash flow drag on the business. |

| Carried interest | Often tiered, with the sponsor’s promote increasing as investor returns cross higher MOIC or IRR thresholds. | Carry determines how upside is shared. A well-structured carry arrangement rewards the sponsor when investors perform well, not merely when a deal closes. |

| Preferred return | An 8% to 9.9% preferred return is a common reference point in many independent sponsor structures. | The preferred return determines what investors receive before sponsor carry begins. It is one of the main protections against the sponsor earning upside too early. |

| MOIC hurdle | Increasingly common as a primary or partial carry hurdle, especially in tiered structures. | MOIC rewards total multiple of capital. A 3.0x deal is treated as a 3.0x deal whether it takes five years or seven years, which can reduce timing pressure on the sponsor. |

| IRR hurdle | Still used in many structures, either alone or alongside MOIC. | IRR penalizes time. If the same 3.0x outcome takes longer, the sponsor’s promote can be reduced or eliminated depending on the hurdle structure. |

| Catch-up provision | Frequently included after return of capital and preferred return, allowing the sponsor to catch up to its agreed share of profits. | Catch-up mechanics can materially change economics. Investors should model the actual waterfall from the operating agreement, not rely on headline carry percentages. |

| Governance rights | Often include information rights, consent rights over major decisions, board observation rights, or approval rights for new debt, acquisitions, and exits. | Governance is downside protection. Minority investors need to know who controls major decisions when the deal performs differently than expected. |

Closing fee. Paid at close of the platform and at each add-on. 82 percent of sponsors structure it as a percentage of enterprise value. 56 percent use exactly 2 percent of EV. Typical dollar amounts run $250K to $500K, with 28 percent of deals above $500K. Most capital partners require the sponsor to roll a meaningful portion back into deal equity. McGuireWoods found roughly 60 percent of sponsors rolled at least 50 percent of the fee, and only 14 percent were required to roll the full amount. The rollover percentage is one of the most negotiated terms in the deal because it is a direct proxy for how much personal capital the sponsor has at risk.

Management fee. Paid annually by the portfolio company. 51 percent of sponsors structure it as a percentage of EBITDA with a floor and a cap. Of those, 69 percent use 5 percent of EBITDA, up from 49 percent in 2019. Dollar amounts typically run $250K to $500K per year. Worth knowing: lenders almost always subordinate management fees to senior debt service, and credit documents can block cash payment during covenant tightness. The fee usually accrues even when it cannot be paid, but the cash flow the sponsor actually sees during difficult periods is more volatile than the headline number suggests.

Carried interest. The sponsor’s share of profits above defined return thresholds, paid at exit. 71 percent of deals use a variable-with-hurdles structure. The sponsor earns a small percentage of profits above the preferred return at lower MOIC levels, then steps up at higher tiers. A typical structure looks like 10 percent up to 2.0x MOIC, 20 percent from 2.0x to 3.0x, and 25 percent or higher above 3.0x. 64 percent of sponsors now earn 25 percent or more at the highest tier, nearly double the 37 percent who did in 2019.

The hurdle structure shift is the trend that matters most. MOIC is now the primary hurdle in 50 percent of deals, up from 27 percent in 2019. Hybrid MOIC plus IRR structures cover another 22 percent. Pure IRR hurdles have fallen to roughly 20 percent. The 8 to 9.9 percent preferred return remains standard. Full catch-up provisions, where the GP catches up to its target promote share before the tier split kicks in, are used in 74 percent of deals.

If you are seeing a deal with terms materially outside these bands, ask why. The annual survey reports, law and accounting writeups, and independent sponsor conferences are useful reference points for what current market terms actually look like.

How a Waterfall Actually Works

The structure is easier to see with real numbers. Say you commit $10M of equity alongside the sponsor. The deal holds five years and exits at 3.0x invested capital, returning $30M gross. Assume an 8 percent preferred return, full catch-up, and tiered carry of 10 percent up to 2.0x MOIC, 20 percent from 2.0x to 3.0x, and 25 percent above 3.0x.

Distributions flow through four stages:

- Return of capital. You get the first $10M back to recover your commitment.

- Preferred return. You receive the 8 percent annual preferred return compounded over five years, roughly $4.7M on the $10M commitment. Cumulative distributions to you: $14.7M. Remaining proceeds: $15.3M.

- Catch-up. The sponsor receives 100 percent of the next distributions until they have caught up to their target share of cumulative profits above return of capital and preferred return.

- Tier split. Remaining proceeds split per the relevant MOIC tier, in this case 25 percent to the sponsor and 75 percent to you.

The exact numbers depend on the operating agreement, and you should model every waterfall directly from the document rather than estimating from headline percentages. But the pattern holds. You see return of capital and preferred return first. The sponsor’s share of profits accelerates as the deal performs better.

The IRR versus MOIC choice is the part most new LPs underweight. Take the same $10M deal at 3.0x in five years, then imagine it takes seven years instead. Under a MOIC hurdle, the sponsor’s promote is identical, because the deal returned the same multiple. Under an IRR hurdle, the preferred return compounds against the sponsor for two extra years, which can wipe out most of the promote or eliminate it entirely. Capital providers historically preferred IRR for exactly this reason. The market has shifted toward MOIC because hold periods have lengthened across all of private equity, and sponsors pushed for terms that did not penalize them for that lengthening. When you are evaluating a deal, know which structure you are agreeing to and what it implies about the sponsor’s incentives on timing.

Debt Matters Most When the Base Case Misses

A capital structure that looks efficient in a spreadsheet can become fragile when QoE lowers EBITDA, rates stay higher, lender terms tighten, or growth takes longer than expected.

Axial’s 2025 report found that traditional senior debt and seller notes were the most prevalent debt instruments used by independent sponsors. Junior debt usage declined from 81.3 percent of deals in 2023 to 60.8 percent in 2025, which Axial read as sponsors taking a more conservative approach to leverage in a higher-rate environment.1 That is a healthy shift.

Prefer a structure that survives a reasonable downside case over one that maximizes the model IRR. A 25 percent projected IRR built on aggressive leverage, perfect add-ons, margin expansion, and multiple expansion is not the same as a 25 percent projected IRR built on modest debt, credible operating improvements, and a conservative exit. The number is not the underwriting. The assumptions are the underwriting.

4. Underwrite the Execution Plan

A value-creation plan should not read like private equity Mad Libs. “Professionalize sales. Improve margins. Pursue add-on acquisitions. Upgrade systems. Add management depth. Optimize pricing.” Those are not wrong. They are just not enough.

A real post-close plan answers questions like: Who is running the company on day one. Is the seller staying, rolling equity, or leaving. What are the first 100-day priorities. What KPIs will be reported monthly. Which operating changes are under sponsor control. Which growth assumptions depend on the market. What hires are required. What systems are missing. What add-on targets have been identified. What happens if no add-ons close in the first 18 months. What breaks the thesis.

A sponsor who cannot explain the downside case clearly has not underwritten the deal deeply enough. The best sponsors do not sell certainty. They show command of the uncertainty.

Why Some LPs Prefer Independent Sponsor Deals to Blind-Pool Funds

For investors who have done both, the structural advantages of sponsor deals are concrete:

- Direct underwriting on a named asset. You evaluate a specific business with real financials, not a manager’s projected pipeline. The diligence work you do is on the asset that produces the return.

- Better alignment. Sponsors typically roll 50 percent or more of their closing fee into equity. They have personal capital in every deal. The carry rewards absolute returns rather than fund-level metrics that can be smoothed across vintages.

- Lower entry multiples. 54 percent of independent sponsor deals close below 6.0x EBITDA, per McGuireWoods. Middle market PE medians sit between 10.2x and 14.9x. Large-cap PE between 11.1x and 13.3x. The lower entry valuations are partly due to smaller deal size and partly to sponsors sourcing founder-owned businesses that have not yet been professionalized and have not been auctioned to institutional buyers.

- The opt-out. A fund commitment locks you in. A sponsor relationship lets you pass on any specific deal that does not meet your criteria. Over time, you build a portfolio of investments you actually wanted to make.

The Risks That Come With the Structure

The same features that produce the advantages also produce the risks. Five matter most:

- Concentration. Each commitment is one business, not a portfolio. Diversification is essential.

- Execution. Deals break between LOI and close. Diligence reveals issues. Financing falls through. Sellers renegotiate. Your time and any out-of-pocket diligence costs are not recoverable.

- Sponsor quality. No fund-level track record across multiple vintages. Even experienced sponsors may have only completed two or three platforms.

- Liquidity. Hold periods run five to seven years with limited interim distributions. No practical secondary market.

- Governance variability. A well-structured deal has clear board observation rights, information rights, and major decision approval rights. A poorly structured one leaves co-investors passive while the lead investor controls everything.

The risks are manageable, but only with eyes open. Investors who treat sponsor deals like fund commitments and skip the deal-level diligence get the worst of both structures.

What the Dedicated Co-Investment Vehicles Mean

The most visible change in the segment over the past two years is the rise of dedicated independent sponsor co-investment vehicles. Global Endowment Management closed its inaugural sponsor fund at over $450M on April 9, 2025, beating a $300M target with another $150M from affiliated vehicles.4 HighVista Strategies closed Fund XI at $800M on February 3, 2026, beating a $725M target.5

These vehicles do several things. They give institutional capital a way into the segment without building direct underwriting capability. They offer diversification at the fund level. And they create a fee benchmark. Management fees in dedicated sponsor vehicles often run below 1 percent versus the 2 percent traditional in committed-fund PE, which is putting pressure on economics across the segment.

The trade-off is that fund-vehicle access reintroduces some of the same blind-pool dynamics direct sponsor investing was designed to avoid. You commit to a portfolio of sponsors the manager selects, not to specific deals. For investors who specifically want direct underwriting on each transaction, these vehicles are a complement, not a substitute.

CapitalPad takes a different approach within the same problem space. Rather than pooling capital in advance, CapitalPad operates as a deal-by-deal private equity co-investment group, sourcing and curating independent sponsor transactions, then aggregating accredited investor commitments into a single SPV per deal. Investors review each transaction individually before deciding whether to participate, with minimums starting at $25,000. Unlike a blind-pool sponsor fund, the structure preserves the deal-level selectivity that makes independent sponsor investing attractive in the first place. Unlike a placement agent, CapitalPad does not charge sponsors a fee for raised capital. Accredited investors can apply for access.

A Practical Investor Checklist

Before committing capital to an independent sponsor deal, you should be able to answer most of the following.

Sponsor

- What relevant deals has the sponsor closed, and how did they perform.

- How did the sponsor source this opportunity.

- Why is the sponsor advantaged in this sector.

- How much sponsor capital is going into the deal, and at what rollover percentage.

- What references from prior capital partners and management teams can be checked.

Business

- What is EBITDA and how reliable is it after QoE.

- How concentrated are customers and how dependent is the business on the founder.

- What capital expenditures are required.

- What is the realistic downside case, not the model downside case.

Structure

- What is the entry multiple and how does it compare to recent comparables.

- How much debt is used, and what are the covenants.

- What fees does the sponsor receive, and how much is rolled into equity.

- Is the hurdle MOIC, IRR, or hybrid, and what is the catch-up provision.

- What consent rights, board rights, and reporting do investors receive.

Execution

- Is the equity fully committed, or are there gaps.

- Is debt financing committed or only indicated.

- Who runs the business on day one.

- What is the first 100-day plan, in specifics.

- What breaks the thesis if it goes wrong.

A checklist will not make a bad deal good. It will help you avoid lazy yeses.

What Good Looks Like

A strong independent sponsor deal usually has a clear pattern. The sponsor has relevant experience. The sponsor is investing meaningful capital. The business is profitable and understandable. EBITDA quality has been tested. The entry valuation leaves room for error. Debt is reasonable. Seller rollover or seller financing supports alignment. Fees are transparent. Carry rewards performance. Governance rights are clear. Reporting is defined. The 100-day plan is specific. The downside case is not ignored. The sponsor can explain why this deal should close and why it should work after closing.

No single factor is enough. Sponsor quality without business quality is not enough. A good company with weak governance is not enough. A strong projected IRR with fragile assumptions is not enough. The best independent sponsor deals work because the sponsor, business, structure, and execution plan fit together.

Independent sponsor investing is not a shortcut around private equity diligence. It is private equity diligence in a more specific format. The model gives you more visibility, more selectivity, and access to profitable lower middle market businesses that are difficult to reach through traditional fund commitments. It also puts more responsibility on you.

Do not underwrite the teaser. Do not underwrite the projected IRR alone. Do not underwrite access as if it were edge. Underwrite the sponsor, the business, the structure, and the execution plan together. The investors who do that work well are getting access to founder-owned businesses on terms the institutional market cannot match. The investors who skip the work are usually the ones who learn the hard way why the work matters.

Frequently Asked Questions

What is an independent sponsor deal?

An independent sponsor deal is a private equity acquisition where the sponsor identifies, negotiates, and signs an LOI on a specific company before raising the equity and debt to close. Unlike traditional private equity, there is no committed fund of capital behind the sponsor. Equity is raised from accredited investors, family offices, and funds on a deal-by-deal basis, typically through a single SPV per transaction. Investors evaluate the actual company, the sponsor, the capital structure, and the execution plan before committing capital.

How are independent sponsor deals different from private equity fund commitments?

A traditional private equity fund commitment is a blind-pool decision. You commit capital to a manager who will deploy it across fifteen to twenty companies over three to five years, and you do not know the actual portfolio at the time of commitment. An independent sponsor deal inverts the order. The sponsor finds the company first and raises the capital second, which means every investor evaluation is on a known asset with audited financials and a defined capital structure. Investors can pass on any specific deal that does not meet their criteria, which produces a more concentrated but more selective portfolio over time.

What returns do independent sponsor deals typically produce?

Return outcomes vary materially by sponsor, sector, and vintage. The structural setup favors better return potential than committed-fund private equity for two reasons. First, entry multiples are lower. 54 percent of independent sponsor deals close below 6.0x EBITDA, compared with middle market PE medians between 10.2x and 14.9x. Second, the deal-by-deal selectivity gives investors the ability to avoid weak deals rather than having them averaged into a fund return. The trade-off is concentration risk. Each commitment is one company, not a portfolio of twenty.

What are typical fee structures in independent sponsor deals?

Three economic components define sponsor compensation. A closing fee paid at close, typically 2 percent of enterprise value, with sponsors usually required to roll at least 50 percent back into deal equity. A management fee paid annually by the portfolio company, typically 5 percent of EBITDA with a floor and cap, usually running $250K to $500K per year. And carried interest paid at exit, typically structured as tiered carry that increases at higher MOIC levels, with 25 percent or more at the highest tier in 64 percent of recent deals. These numbers come from the 2024 McGuireWoods Independent Sponsor Deal Survey and the 2025 Citrin Cooperman Independent Sponsor Report.

What minimum investment is required for an independent sponsor deal?

Minimums vary by sponsor and capital partner. Direct investment with a sponsor on a one-off deal can require six- or seven-figure commitments depending on the size of the equity raise and the sponsor’s preferences. Co-investment groups have lowered the floor significantly. CapitalPad, for example, aggregates accredited investor commitments into a single SPV per deal with minimums starting at $25,000, which makes deal-by-deal sponsor investing accessible to individual accredited investors and smaller family offices who would not otherwise have reasonable access to the segment.

How do investors access independent sponsor deals without sourcing them directly?

Three channels exist. Direct relationships with sponsors require building a network of operators and showing up at events like the annual McGuireWoods Independent Sponsor Conference and the iGlobal Forum summits, which takes years and a meaningful time commitment. Dedicated co-investment funds like Global Endowment Management’s $450M sponsor fund and HighVista Strategies’ $800M Fund XI offer pooled exposure, with the trade-off of reintroducing blind-pool dynamics. Co-investment groups like CapitalPad sit between the two, sourcing and curating individual deals and giving investors the choice to participate transaction by transaction at lower minimums than direct sponsor relationships typically require.

References

- Axial. 2025 Independent Sponsor Report.

- Citrin Cooperman. 2025 Independent Sponsor Report and related Uncharted No More series.

- McGuireWoods LLP. 2024 Deal Survey of Independent Sponsor-Led Transactions.

- Global Endowment Management. GEM Closes On Over $450 Million for Inaugural Independent Sponsors Fund. April 9, 2025.

- HighVista Strategies. HighVista Closes Oversubscribed Private Equity Fund XI at $800 Million. February 3, 2026.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, tax, or financial advice. Independent sponsor deals involve significant risks, including loss of capital, illiquidity, and concentration. Past performance and market conventions discussed here do not guarantee future results. Any investment decision should be made in consultation with qualified advisors and based on the specific facts of the opportunity under consideration. CapitalPad does not make investment recommendations through this content.